Ithmaar Bank aspires to the highest standards of ethics. This aspiration defines the entire industry. Islamic banking, in its simplest terms, is banking with a bigger emphasis on ethics.

Islamic Banking system is based on Islamic Sharia principles. All transactions in Islamic banking must follow the relevant Sharia rules, called Fiqh Al- Muamalat. The main two sources of Islamic banking rules are the Quran and Sunnah. Islam prohibits the collection of interest (Riba/ Usury) and allowes trading which based on buy and sell concept and profit and loss sharing. (وَأَحَلَّ اللَّهُ الْبَيْعَ وَحَرَّمَ الرِّبَا ۚ) Al-Baqarah 275

Some of the prohibited transactions as per Sharia principles are:

- Riba (Interest/Usury)

- Gharar (Uncertainty/ Deception)

- Maysir (Gambling)

- Bai Al Inah

- No hidden fines, fees or charges

- Asset- backed investments and no speculation

- Sharia-compliant with an absolute and unconditional commitment to ethical investments

- Additional layer of supervision, with Sharia supervisory board

- Risk-profit sharing business model

Ithmaar Bank offers its customers a variety of Islamic banking products. The type of products are as follows:

Murabaha

Murabaha is one of the most common products used by Islamic banks.

It is the sale of a commodity at the price that the seller bought, with the increase of a known agreed profit, at a rate of the price or a lump sum.

The selling price and the mark-up have to be clearly determined in advanced and the commodity has to be exist at the time of signing the contract. At Ithmaar Bank, Murabaha is used in Auto Finance, Real-Estate Murabaha and Personal Finance Tawarruq.

Ijarah

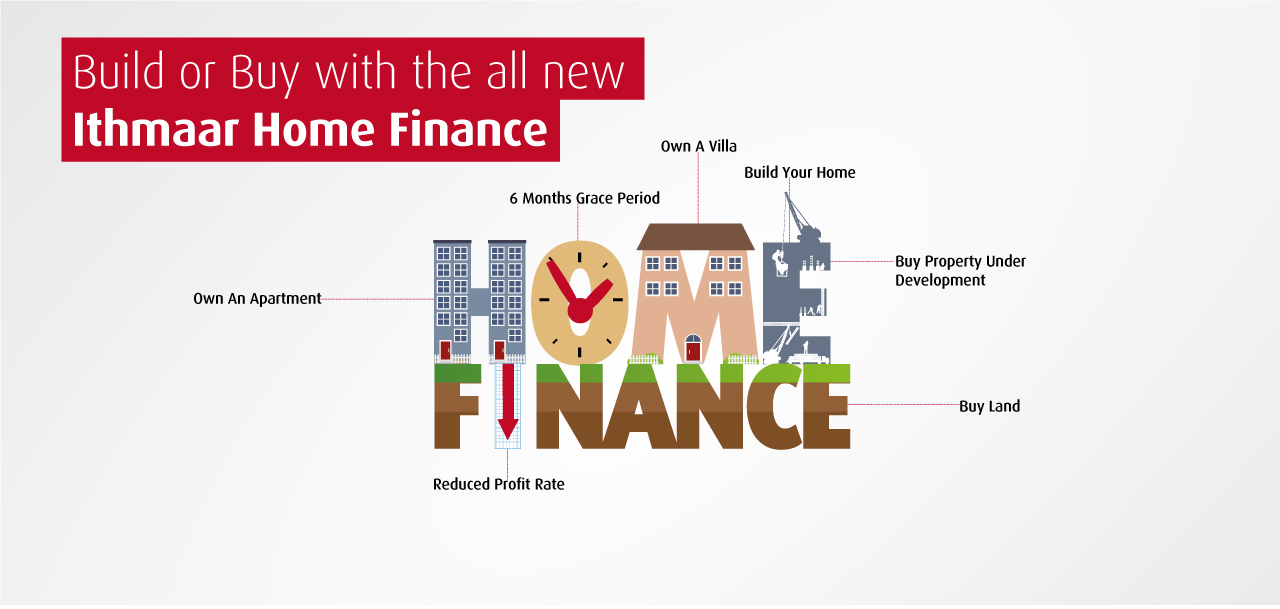

Ijarah is a contract for the purpose of ownership of a legitimate benefit, for a period known to a member of the project. At Ithmaar Bank, Ijarah is used in Home Finance.

Modaraba

Modaraba is a partnership, wherein one party provide the capital (Rab Al Mal) and the other party will use it in investments (Mudarib). The profit will be shared based on agreed percentage in advanced. At Ithmaar Bank, Modaraba is used in Saving Accounts and Deposits.

Wakalah

Wakalah is the assignment of someone else to develop his money with wages or without wages , where one party (the customer) delegates another party (the bank) to act on his/her behalf in a permissible matter of delegation for a known remuneration as a lump sum or a specific amount of income.

Comparison between systems in Islamic Banking and conventional banking include:

| Islamic Bank | Conventional Bank | |

|---|---|---|

| 1 | The structure of Islamic banks requires a Sharia Supervisory Board to review and ensure that all transactions are in line with Sharia principles. | The structure of conventional banks does not require a Sharia Supervisory Board to review and approve banking transactions. |

| 2 | Islamic banking transactions are asset based. | Conventional banking transactions are money based. |

| 3 | Islamic banking is based on trading. | Conventional banking is based on interest. |

| 4 | Islamic banking transactions are free from Riba (interest), Gharar (uncertainty) and Maysir (gambling). | Conventional banking might have elements of Riba, Gharar and Maysir. |

| 5 | Additional fees may not be charged on defaults or late payments. Penalty charged must be given away as charity. | Additional fees may be charged on defaults or late payments |

| 6 | Islamic banking rules follow Quran and Sunnah. | Conventional banking rules are man-made. |

| 7 | Deposits are invested in Sharia permissible ways through Murabaha, Ijarah, Musharakah… etc. The profits generated are shared between the bank and the customer. | Deposits are from long-term or short-term loans. The customer is the lender, who gets interest based on the period of the deposit/loan. |